There is a version of the AI-native services pitch that goes like this: pick a fragmented professional services category, raise enough capital to roll up three or four traditional players, layer AI on top, and you have a $50M ARR business in eighteen months. It sounds clean. It is the kind of plan that gets a lot of nods in a room full of people who think in spreadsheets.

I want to make the case that it is mostly wrong, or at least wrong as a starting move. Building organically is harder in the first two years and almost always faster to durable scale after that. The mistake founders are making right now is treating inorganic ARR as a shortcut when it is closer to a tax: cheap to acquire, expensive to keep, and difficult to compound on top of.

A note on terminology before going further. We coined the term "AI-Native Services" (AINS) at Emergence to describe a specific kind of company: one built from day one to deliver a professional service through an AI-first operating model, not a traditional services firm with AI bolted on. The distinction between organic AINS and AI-flavored roll-ups is exactly the distinction this piece is about, and it is the reason we needed a name for it.

The roll-up logic usually rests on a tell

The most common reason founders reach for a roll-up is customer acquisition. The pitch sounds reasonable: services categories are relationship-driven, distribution is hard, buying a book of business is faster than building one.

The problem is that the best AINS companies do not actually struggle with customer acquisition. For example, Harper Insure, an AI-native insurance broker, has to throttle inbound demand because they can’t yet service it all. Or Hanover Park, which does fund administration for private markets, hit the same constraint: more inbound from GPs than they could staff against. The bottleneck at each of these companies is almost never demand. It is supply: hiring enough adjusters, brokers, fund accountants to deliver on the demand they are already generating. Customers find them, refer them, switch to them, because the product is meaningfully better, faster, or cheaper than what they had before.

This has a sharper implication than it sounds. If you are AI-native and you are struggling to win customers in a market where almost none of your competitors are AI-native, the most likely explanation is not that distribution is hard. It is that you are not actually AI-native enough, meaning the product is not yet good enough to win on its merits. For at least the next year or two, while incumbents are still figuring out how to incorporate AI, winning customers should be the easy part if the product is right. If it is not, a roll-up does not fix the problem. It cements it. You have papered over a product gap with acquired revenue and added a workforce that will make it harder, not easier, to close that gap.

The identity problem

A roll-up's culture is the weighted average of what you bought. If you acquire two hundred traditional accountants and add twenty AI-native ones, you are a traditional accounting firm with an AI veneer. The math does not care about the deck.

This matters because in AI-native services, you are selling the outcome. Not software, not a tool. The outcome. Outcome quality is produced by people and the systems they build around themselves. If most of your people learned their craft in a pre-AI world and most of your systems were built to manage them, your outcomes will look like everyone else's outcomes, slightly faster.

There is also an operational version of this problem that compounds the cultural one. Running an acquired traditional services business is a full-time job. It demands attention from your executives, your engineers, your operators .Every hour spent keeping that legacy business running is an hour spent reinforcing the habits, expectations, and rhythms of a traditional firm. Identity is shaped by what those people spend their day doing, and what they spend their day doing in a roll-up is mostly running a traditional services business.

AI-native practitioners are the unlock, and most founders are underestimating them

The single most important hiring decision in an AI-native services business is whether your practitioners are themselves AI-pilled. By practitioners, I mean the people who actually deliver the service: the claims adjuster, the insurance broker, the fund accountant, the lawyer.

Across our AINS portfolio, we have seen practitioners who genuinely live and breathe AI tools deliver three to ten times the throughput of their non-AI-native counterparts on comparable work. This is a directional range from what we have observed across portfolio companies, not a published benchmark, and the spread depends on the task. But the magnitude is consistent enough that it should change how founders think about hiring.

A few implications follow.

First, and most obviously, your headcount plan is much smaller than a traditional services firm's plan, which means your margins look better at every stage of growth. Second, your hiring funnel is not a bottleneck on revenue in the way it is for traditional firms, which means you can take a customer commitment without immediately panicking about staffing it. Third, and this is the one founders miss, the gap between an AI-native practitioner and a traditional one is wide enough that mixing them in the same org creates real cultural friction. The AI-native ones will get frustrated. The traditional ones will feel watched.

The practical implication for founders building organically is that you should be ruthlessly selective about who delivers the service in your first hundred clients. The product feedback loop in an AI-native services business runs through your practitioners. If they are not the earliest adopters of AI in your category, you are getting product feedback from people who do not understand what is possible, which means you are building the wrong product.

The implication for founders thinking about acquiring is harder. You are not just buying revenue. You are buying a workforce whose habits, tools, and self-image were formed in a different paradigm, and you are taking on the change management cost of moving them. That cost is large, slow, and frequently underestimated as it’s really hard, if not impossible, to truly know pre-acquisition.

Leakage, and why acquired ARR is not your ARR

The other underappreciated cost of inorganic growth is leakage. Customers acquired through acquisition churn at rates that founders consistently underestimate, for reasons that are structural rather than executional.

Two kinds of stickiness anchor a professional services book of business. Process stickiness is built on workflow integration: the firm knows your systems, your data, your reporting cadence. Relationship stickiness is built on personal trust: a specific partner has known the client for years.

Process stickiness is collapsing. AI lowers the cost of re-platforming a client onto a new firm's workflow from a multi-month project to a multi-week one. The thing that used to lock customers in, the cost of moving, is going down across almost every professional services category at the same time. If your acquired ARR is held in place primarily by process inertia, expect more churn than the seller's historical numbers suggest.

Relationship stickiness is the harder one to think about, and the one founders are most likely to overestimate. The mistake is assuming that because relationships were a moat in the past, they will be a moat in the future. A lot of what we call relationship loyalty is actually the absence of a meaningfully better alternative.

I had the same insurance broker for most of my adult life. I liked him. I trusted he was doing his best. But every insurance broker I had ever met was equally mediocre, and the cost of switching was not obviously worth the upside. That is not a relationship moat. That is inertia wearing a relationship moat's costume. Once a company like Harper can deliver a customer experience that is ten times better, the relationship reveals itself as what it actually was, which was a tie I had not had a reason to question.

There are deep relationships and there are not-so-deep relationships, and founders evaluating an acquisition should be eyes wide open about which kind they are buying. A book of business held together by genuine, multi-decade trust between specific people will probably travel. A book of business held together by "no one else has been notably better" will not, and that is most books of business. AI is the thing that finally gives those clients a reason to look elsewhere.

The net effect is that the moats around inorganic ARR are weaker than they look. The process moat is dying because of AI. The relationship moat is mostly inertia, and inertia is exactly what a meaningfully better product breaks.

Pricing lock-in and the trap of legacy economics

Acquired books of business come with contracts, and contracts are cages. Consider a BPO processing paperwork for medical practices at $100k per year on a multi-year deal. An acquirer can deploy AI to do that work with fewer humans, which improves margins. But the contract prevents capturing the additional value delivered, such as doing the work faster and with fewer errors. The upside accrues to the customer, not the business.

An organic builder faces none of that drag. Built AI-first from day one, they can go to the same medical practices and price closer to the value they actually generate: per document, per outcome, at a scope the legacy player was never positioned to offer. The AI thesis in a roll-up improves your costs. The AI thesis in an organic build expands your revenue ceiling. Those are different businesses.

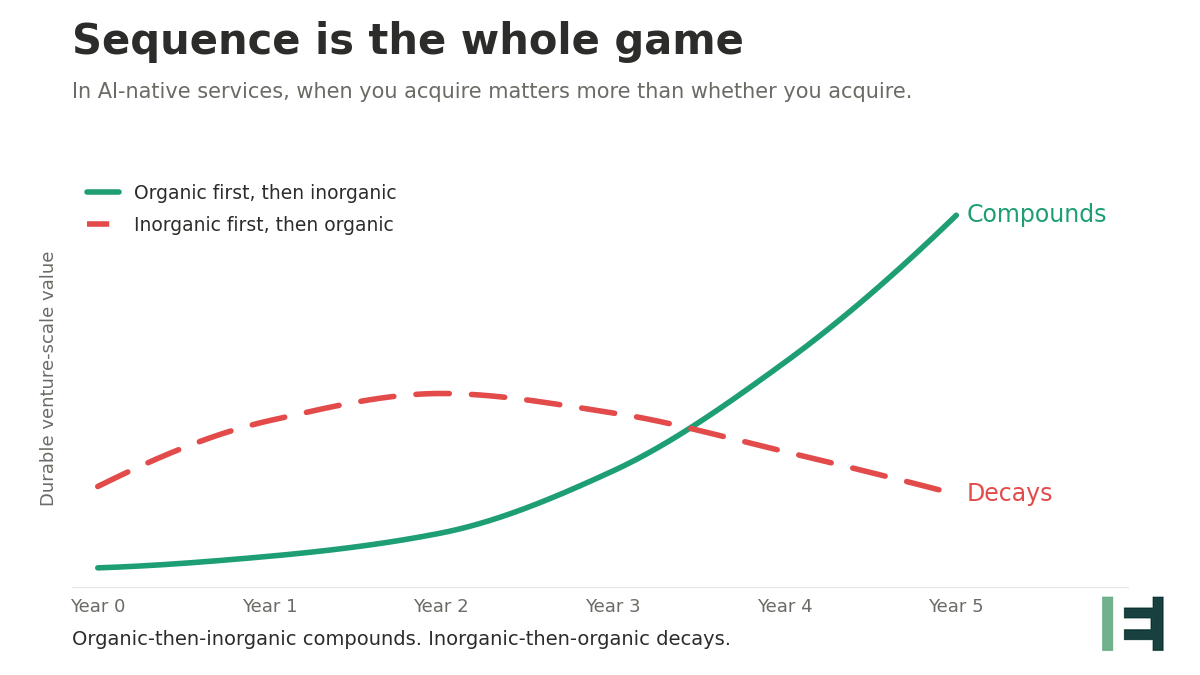

Sequence matters more than founders are treating it

None of this is an argument that acquisitions are wrong in AI-native services. It is an argument that sequence matters more than founders are treating it.

Organic-then-inorganic is a much easier game than inorganic-then-organic. Once your platform is real, your culture is solidified, and your AI-native practitioners are setting the standard for how the work gets done, an acquisition becomes an accelerant. You are bringing acquired teams into a system that has gravity. They conform to you.

Inorganic-then-organic is the opposite. You spend the first two years absorbing teams whose habits run against your thesis, and you build culture in their gravitational field rather than your own. By the time you try to retrofit AI-native practices on top, the cement has set.

There is also a real risk of dying of indigestion. Founders underestimate how badly a too-large or too-different acquisition can break a young company. The integration consumes engineering attention, executive time, and culture-shaping bandwidth at exactly the moment those resources should be compounding into product. I have watched promising AI-native services companies lose a year to a single acquisition that looked accretive on a model and turned out to be a tar pit.

What building right actually looks like

The version of organic that wins is not slow. It is disciplined. What that looks like in practice, from hiring your first AI-native practitioners to building the platform from inside the work to knowing when you have earned the right to scale, is what the Emergence AINS Playbook is built around. The short version is this: a small team delivering an outcome meaningfully better than what incumbents produce, earning brand and trust through outcome quality rather than relationships purchased on a balance sheet. AI-native services are unlikely to be winner-take-all categories, which means the durable differentiation is going to be brand, customer experience, and perceived outcome quality. Those are things you build. They are not things you buy.

If you build that foundation right, acquisitions become a tool you can use later from a position of strength. If you skip it, you will spend years trying to graft an AI-native identity onto something that has already decided what it is.

The short version

- If customer acquisition is your reason to roll up, it is probably also evidence that the product is not yet AI-native enough. Fix the product first.

- Identity in a services business is the weighted average of who delivers the work and what they spend their day doing. Roll-ups make both of those things traditional.

- Acquired ARR leaks. Process stickiness is dying because of AI; relationship stickiness is mostly inertia, and a better product breaks inertia.

- Acquired books come with legacy pricing baked in, exactly when AI lets you escape it.

- Organic-then-inorganic compounds. Inorganic-then-organic decays. Sequence is the whole game.